From Strategy Signal to Live Trade

Backtests are useful, but live trading has one extra layer: the signal has to arrive, the trader has to see it, and the broker fill has to land close enough to the strategy report to make the setup realistic.

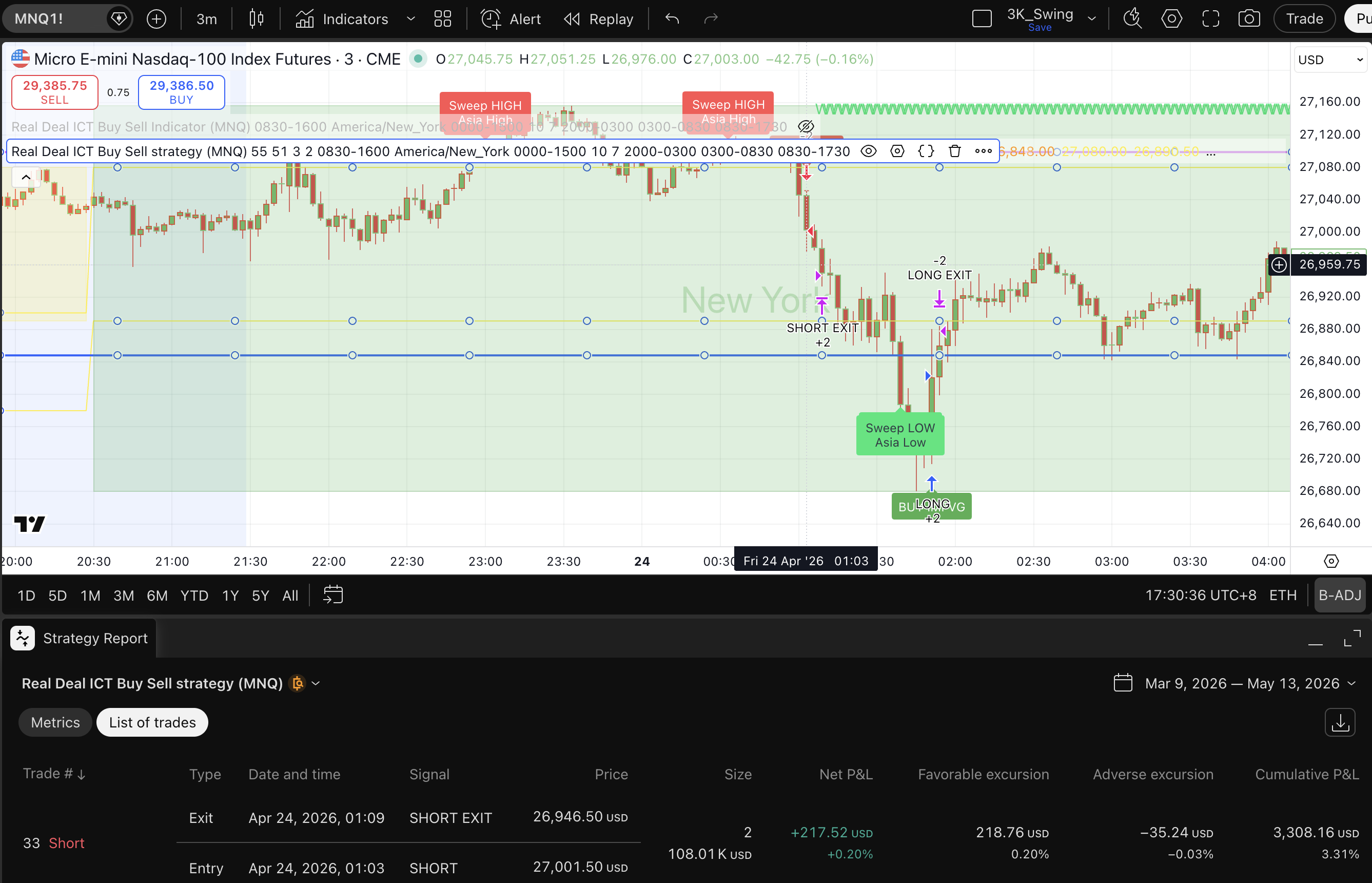

On April 24, 2026, RivetAlgo gave a short signal on MNQ using the Real Deal ICT Buy Sell Strategy (MNQ) and matching indicator alert. The setup appeared on the 01:03 3-minute bar, the alert fired at the bar close around 01:06, and the live TopstepX trade was entered at 01:06:03.

This example is useful because the TradingView strategy result and the live funded-account result were close. The strategy report used MNQ cost simulation, including 0.62 USD commission per side and a few ticks of slippage, so the report was not pretending live trading has perfect fills.

The Live Setup Used Indicator and Strategy Together

The indicator alert and strategy were both loaded on the MNQ 3-minute chart. The indicator was responsible for the live alert message, while the strategy report recorded how the same rule set behaved on TradingView.

This matters because indicator alerts and strategy reports answer different questions. The alert says, "pay attention now." The strategy report says, "under the configured strategy rules, this is how the trade measured."

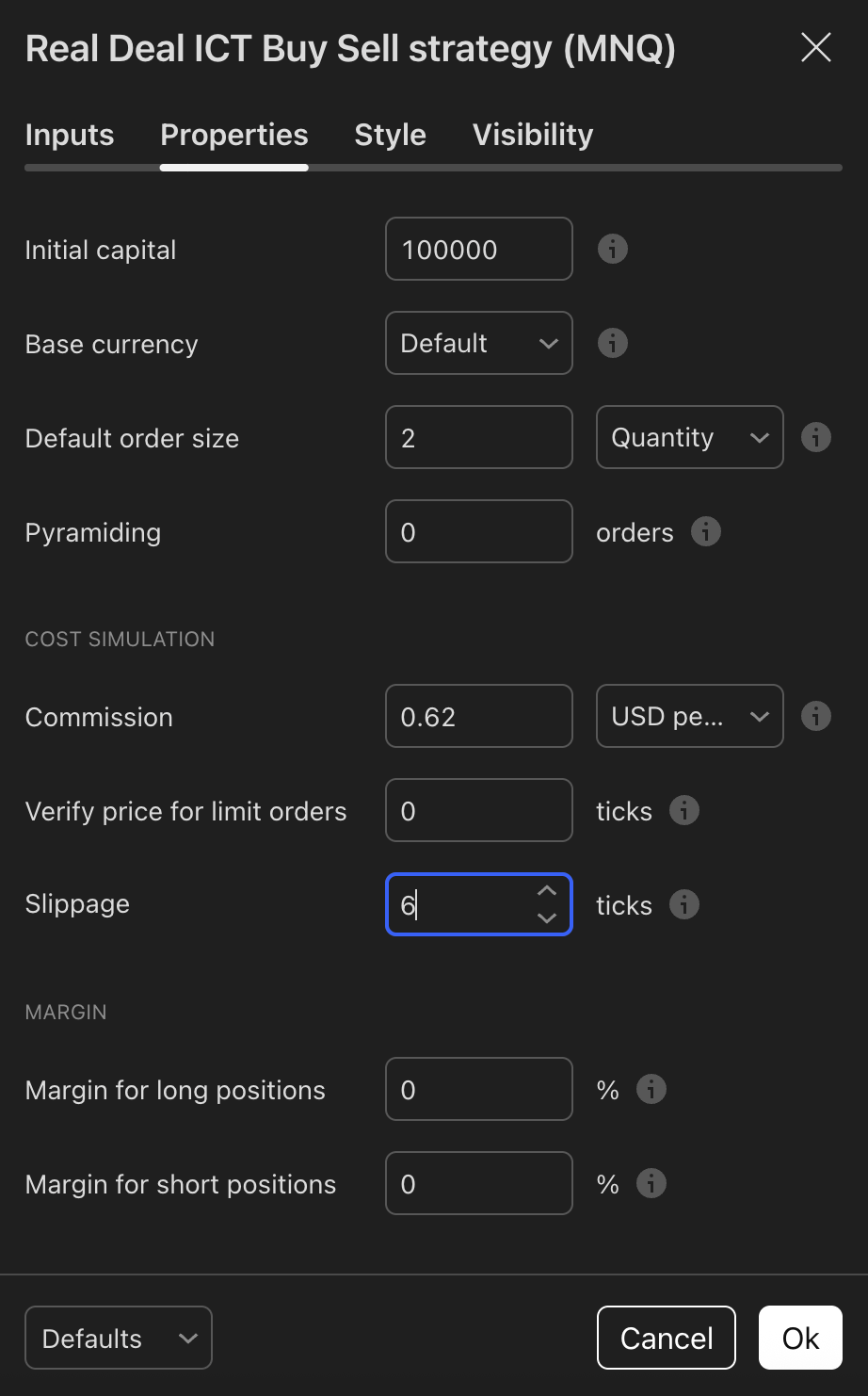

Cost Simulation Was Set Before the Trade

RivetAlgo's strategy report is only useful if it is not too clean. For this example, the strategy properties included a 2-contract order size, MNQ-style commission, and slippage. That makes the TradingView report easier to compare against a real TopstepX execution.

It will never match live trading perfectly. Broker routing, spread, fill timing, platform latency, and manual reaction time can all change the result. But the goal is to make the strategy report honest enough that the live result can be compared against it.

The Alert Fired at the 3-Minute Close

The short signal was on the 01:03 3-minute bar. On TradingView, that does not mean the confirmed signal was tradable at 01:03. It means the candle started at 01:03 and closed at 01:06.

The alert was already set before the trade. When the 01:03 candle closed, the alert fired at 01:06:00. The live trade was then taken almost immediately at 01:06:03.

The Live TopstepX Trade

The live short was entered at 01:06:03 and closed at 01:10:01 for a 56-point move on 2 MNQ contracts.

A 56-point move on MNQ equals roughly 112 dollars per contract, or 224 dollars gross before the platform's fee and execution adjustments shown in the account row.

The Strategy Report Was Close to the Live Result

TradingView recorded the strategy short entry on the 01:03 bar at 27,001.50 and the strategy exit on the 01:09 bar near 26,946.50. The reported net result was +217.52 USD after the configured cost simulation.

The live TopstepX fill was slightly different: short at 27,002.00, exit at 26,946.00, and +224.00 USD gross before the visible fee and cost adjustments. That difference is normal. The important point is that the real execution and the strategy report were measuring the same trade idea.

| Source | Entry Reference | Entry Price | Exit Reference | Exit Price | Result |

|---|---|---|---|---|---|

| TradingView strategy | 01:03 bar | 27,001.50 | 01:09 bar | 26,946.50 | +217.52 USD net |

| TopstepX live fill | 01:06:03 | 27,002.00 | 01:10:01 | 26,946.00 | +224.00 USD gross |

What This Shows About Live Workflow

This was not automation placing the order. This was a trader using RivetAlgo as the decision system: the chart produced the signal, the alert delivered the timing, and the trader acted quickly after the confirmed 3-minute close.

- The strategy and indicator were already loaded before the setup happened.

- The alert was set before the trade, so the signal did not depend on watching every tick.

- The 01:03 bar had to close first, so the live action happened around 01:06.

- The live order used a market fill for speed; limit orders can prioritize price.

- The strategy report used commission and slippage assumptions to stay close to real execution.

This is the bridge between strategy research and live trading. The trader still controls the account, but the process is less emotional because the alert and strategy logic are doing the heavy filtering first.

The Takeaway

Live trading with RivetAlgo is more than a chart label. The workflow is signal, alert, confirmed 3-minute bar close, execution, and comparison against the TradingView strategy report.

In this MNQ example, the short signal came from the 01:03 bar, the alert fired at 01:06, and the live trade entered at 01:06:03. Because commission, slippage, and cost simulation were already included, the funded-account result stayed closely aligned with the strategy report.

That is the goal: a setup where backtested results and live execution can match closely, and sometimes perform even better depending on the actual fill.

Use the Playbook to understand how strategy logic behaves before, during, and after live execution.